Glossary of Tax Terms

A list of definitions of tax terms individuals and businesses need to know while processing tax returns during tax season.

If you’re not an accountant, then it’s easy to get a little confused by all the different tax jargon and specialised terminology.

Having a good tax consultant (such as those on our team here at H&R Block) is a good way to avoid stress, as they will help you make sure you understand all the important things, don’t miss out on any possible benefits and avoid any possible issues or penalties. But it also helps to have your own basic knowledge – so we’ve put together this helpful glossary of common tax terms you might come across when doing your taxes:

Assessable income – This is any money you receive during the tax year from working or from an investment. It can include salary and wages, tips, allowances, interest, dividends, bonuses, commissions and rent. You are not usually required to pay tax on gifts or prizes, or on some government pensions and payments (although this can vary, so if in doubt, check with your accountant).

Australian Business Number (ABN) – This is a unique 11-digit number issued by the Australian Business Register (which is operated by the ATO) that identifies your business. All businesses in Australia are required to have an ABN, and it makes things much easier when dealing with the ATO on all tax-related matters. It is free to register for an ABN, but if you use an accountant to complete the application then they may charge a small fee for their services.

Australian Tax Resident – An Australian resident for tax purposes is someone whose usual place of abode is in Australia. You don't need to be an Australian citizen or a permanent resident for immigration purposes to be considered a tax resident. Your tax residency status can impact the amount of tax you pay, and it can change depending on your circumstances, so it is worth consulting a tax expert if you have any doubt.

Business Activity Statement (BAS) – All businesses in Australia that are registered for GST need to lodge a BAS to report on the amount of GST you have collected and paid, as well as PAYG instalments and other taxes. It is usually filled out quarterly, but it can also be done monthly or annually depending on the size and turnover of your business.

Capital Gains Tax – This is a tax paid on any income that is due when you sell any asset (such as shares or property) and make a profit. It is treated as part of your overall income, so the amount of tax you pay depends on which tax bracket is relevant to you. This tax is typically reduced by 50% when you have owned the asset for more than 12 months, and there are some exemptions (for example, you do not need to pay CGT when selling your family home).

Cash flow – This is the net balance of money coming into and going out of a business at any one time. It is usually summarised in a cash flow statement, which is a financial report of where money is coming from (for example, from sales) and going to (for example, to pay salaries) in a business. Positive cash flow means more coming into the business than going out, and negative cash flow means more money is going out than in.

Contractor – This is an individual who performs work for others through their own business, either as a sole trader or in their own company, partnership or trust. Work is usually performed for set terms or periods of time. A contractor needs to have an Australian Business Number (ABN), pays their own taxes and super, and is not entitled to paid sick or injury leave.

Family tax benefit – This is a payment from the government to assist eligible families with the cost of raising children. The amount depends on your income, the number of children in your charge and their ages.

Franked income – When you own shares in a company, you may receive a piece of the company’s profit and this is called a dividend. When the company pays income tax on the profits out of which this dividend has been paid, the company can pass on what are called ‘franking credits’ for this tax payment. This system is called ‘imputation’. You are then able to use these franking credits as tax offsets.

Fringe Benefits Tax (FBT) – This is a tax that employers pay on any benefits given to an employee in addition to their salary or wages, separate to income tax. It could include benefits such as being provided with a work car, access to a discounted loan, paying school fees or salary sacrifice arrangements. It is calculated on the taxable value of the fringe benefit and employers can generally claim an income tax deduction for the cost of providing these benefits, as well as GST credits.

Gift deductible entity – This is an organisation, agency or fund that has been approved by the ATO as eligible to receive tax deductible gifts or contributions. This means that whenever someone makes a donation to one of these entities, they are able to deduct the amount of the donation from their taxable income when lodging their annual tax return for that year.

Gross income – This is the total amount of all income you receive in a set financial year before any deductions have been taken out. The amount that is left after deductions and taxes have been taken out is known as net income.

GST – Goods and Services Tax is a value added tax of 10% that is added to nearly everything you buy in Australia. This means pretty much all goods, services, and other items sold or consumed, with a few exceptions (including some food items, education resources, medical services and financial products). Businesses in Australia need to register for and then collect GST on sales. They can also claim back GST on purchases (so-called ‘input credits’). The net amount is then paid to the ATO when businesses complete their taxes.

HECS – This is the acronym for the Higher Education Contribution Scheme, which is the system for collecting tertiary education (ie any study post-high school). Under this scheme, eligible students who have a Commonwealth-supported place (and are not full fee paying) can access a HECS-HELP loan from the Australian government to pay for any subjects they take as part of their higher education. Once you have graduated or withdrawn from studies, and are earning over the compulsory repayment threshold (for the 2021-22 income year this is $47,014) you will need to make repayments on this loan through your annual tax return.

Imputation credits – When Australian companies pay dividends to their shareholders, they will have already paid tax on the profits out of which the dividends were paid. These taxes can be attributed (or ‘imputed’) to the shareholders as a tax credit, which can be used to reduce their income tax payable.

Income statement – This is a summary that you receive from the ATO in their online services through myGov that includes all of your pay, tax and super information from the previous financial year and will be pre-filled in your tax return. Previously it was given to you by your employer as an ‘income statement’ or ‘group certificate’, and in some cases you may still receive this. But most employers now report directly to the ATO, so most people will receive an income statement.

Income Tax – This is the tax you pay to the government each year on all forms of income, including wages, business profits and investment returns. It can also apply to income that comes from the sale of assets such as a property or shares.

Invoice – This is a record of purchase given to customers when they pay for goods and services, and includes the type of product/service provided, the quantity and the agreed price. If a business is registered for GST then they must provide a ‘Tax invoice’ that details the amount of GST due for each item.

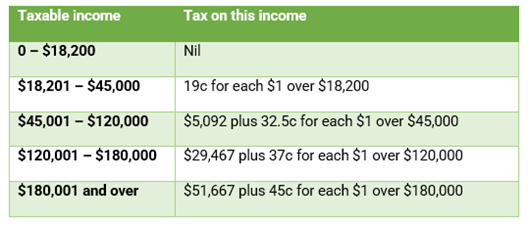

Marginal tax rate – This is the highest rate of tax that you will pay on your income, and it only applies to the portion of your taxable income that falls within your highest tax bracket, not your whole income. Here is a summary of the current tax rates in Australia:

Source: ATO. Taxable income and tax figures are applicable for the year 1 July 2020 to 30 June 2021.

Medicare levy – This is an amount of money collected in the same way as income tax that goes towards funding the public health system in Australia. The amount is usually 2% of your taxable income, although some people may pay less or none at all, depending on their circumstances. If you earn over a certain salary threshold and do not hold adequate private health insurance, you may also need to pay a Medicare levy surcharge of up to 1.5%.

Non resident – Also known as a Foreign Resident, this is someone who has come to Australia but is not considered an Australia tax resident. Foreign residents have no tax-free threshold and do not need to pay the Medicare levy, but they still need to lodge a tax return declaring any income sourced in Australia.

Pay As You Go (PAYG) withholding – Each time you’re paid by your employer they are required to keep a certain amount of tax from each payment and to pass this on to the ATO. The goal is to reduce the chance of you having a huge tax bill at the end of the year, as it has been taken progressively from your pay. When you lodge your tax return for that year, the ATO will assess the amount of tax you have paid compared to the amount you should have paid once other factors are taken into account, such as deductions. Any excess taxes will be returned to you as a tax refund.

Receipt – This is a document that acts as a proof of purchase, and it must always be provided for sales of over $75 or if it is requested by the customer. If can be printed or handwritten, and it must contain the company’s ABN or ACN, plus the date of sale and details of the product or service including price.

Salary sacrifice – This is an arrangement between an employer and employee in which the employee agrees to give up part of the future salary or wages in return for benefits of a similar value, such as a car, property or super contributions. This is sometimes also referred to as salary packaging, and the main benefit is a reduction in your taxable income.

Self employed – This covers anyone who earns business income but doesn’t work as an employee for someone else. Anyone who is self employed needs to register for an Australian Business Number (ABN), pay their own taxes and manage their own super.

Sole trader – This is when an individual operates a business entirely on their own. It’s the simplest and cheapest way to run a business in Australia, as you are the only owner and have total control – but this also means you have full legal responsibility for the business.

Superannuation – This is an amount of money set aside while you are working that will give you an income stream when you retire. Your employer pays 10% of your salary into your nominated super fund, and this fund will then invest the money on your behalf to help the balance grow. You can access the funds on retirement, or under special conditions such as a terminal medical condition.

Super guarantee – This is the minimum percentage of your earnings that must be paid by your employer into your nominated superannuation fund. The rate is currently 10%.

Taxable Income – This is the income you have to pay taxes on, and you can calculate it by subtracting any allowable deductions from your assessable income. The amount that remains is your taxable income.

Tax agent – This is a type of accountant who specialises in the area of taxation, and any related laws. It is important to only ever work with a registered tax agent who is listed by the Tax Practitioner’s Board (TPB) and licensed to help individuals and businesses complete their taxes.

Tax amendment – If you discover you have made a mistake on your tax return, such as forgetting to including some income or deductions, you can always file a tax amendment, which is essentially a correction. It is better to wait until you receive notice from the ATO that your original return has been processed before you file an amendment, as this will help to minimise processing delays. If you are in doubt about whether to file an amendment, you should consult your accountant or tax agent as soon as possible and they will advise you.

Tax audit – This is when the ATO takes a detailed look at your individual tax return and deductions, or your business taxes and BAS, to make sure everything is accurate and the amount of tax paid is correct. You may be selected for an audit due to triggering a ‘red flag’, such as an unusually high number of deductions, or it might be random, and the audit can go back two years for individuals and up to four years for businesses. It can be a stressful process for anyone, but you don’t need to worry if you have kept good records and stuck to legitimate deductions and claims.

Tax avoidance – This is the process of legitimately minimising taxes owed to the ATO through methods that are recognised in tax law, such as taking advantage of all legal deductions and making superannuation contributions. A good accountant can help you identify these legal ways to reduce your annual tax liability, but it is crucial you work with someone you trust to make sure you don’t commit tax evasion.

Tax concessions – These are a variety of benefits, such as flexible payments and reporting options, available to businesses in Australia if they meet certain criteria, such as an annual turnover of less than $50 million or charity/not-for-profit status. To find out if your business qualifies for any tax concessions, speak to your registered tax agent.

Tax Deductible – When you are doing your annual tax return, you are allowed to claim deductions for any expenses that are directly relating to your job, provided you paid for it yourself and can provide proof of purchase (usually a receipt). Eligible deductions vary between professions and it is worth getting the assistance of an experienced tax consultant when checking your deductions to make sure you don’t miss any that are relevant to your work as you could be leaving money on the table unnecessarily.

Tax evasion – This is the illegal practice of not paying taxes that are rightly owed, whether these are income taxes, employment taxes or sales taxes. This can include filing false claims, not reporting income or engaging in contrived tax schemes. The punishments for tax evasion and tax fraud can include fines, community service and even prison time.

Tax File Number – This is your unique personal reference number for Australian taxes and superannuation, and it is essential for filing your annual tax return, accessing government benefits and making voluntary super contributions. It is provided by the ATO free of charge and you have the same tax file number your whole life.

Tax invoice – If a business is registered for GST then they must provide a ‘tax invoice’ that details the amount of GST due for each item sold, in addition to the type of product/service provided, the quantity and the agreed price.

Tax lodgement – This is the process of submitting your tax return to the ATO at the end of each financial year. It should be lodged by 31st October if doing it yourself online or on paper, or you can lodge after this date if you are registered with a tax agent. If you are behind in lodging a tax return, you should contact a tax agent as soon as possible to avoid or minimise possible penalties.

Tax offsets – These are rebates provided to individuals and businesses under certain circumstances that reduce the amount of tax you need to pay. Examples include the private health insurance offset, seniors and pensioners offset and super-related offsets. In general, offsets can reduce your tax payable to zero, but on their own they can't get you a refund.

Tax rate – Australia has a progressive tax system that means the amount of tax you pay changes depending on how much you earn. If you earn under $18,200 in a financial year, you are below the tax-free threshold and do not need to pay any tax. Once you earn over this amount, you are liable to pay tax and the amount increases up to 45% for the highest bracket of earners.

Tax refund – After lodging your annual tax return, the ATO will assess whether you have paid the correct amount of tax in the relevant financial year. If you have paid too much, then you will receive the difference back in the form of a cash tax return. If you have paid too little, then you will be given a bill for the amount owing. The average Australian tax refund is $2800.

Tax return – This is a form that most individuals in Australia need to fill out each year that tells the ATO how much money you have earned in the year and if you are claiming any deductions. It can be filled out online, on paper or via a tax agent, and the ATO use it to assess whether you have paid the right amount of tax, whether you need to pay a Medicare levy or surcharge, and whether you’re eligible for any tax offsets. Once this assessment is completed, you’ll receive either a tax refund (if you paid too much) or a bill for any additional tax owing.

Tax withheld – This is the amount of tax that is kept by your employer each pay cycle and passed on to the ATO. The amount depends on the relevant tax rate for the amount you earn. See Pay As You Go (PAYG) withholding or speak to your tax agent for more information.

Temporary resident – If neither you nor your partner are an Australian citizen, and you are in Australia on a temporary visa, then you will qualify as a temporary resident. This means you will only need to declare any income derived in Australia or earned from employment overseas while you are a temporary resident of Australia, but any other foreign income and capital gains does not need to be declared.

Unfranked dividends – Shares can be fully franked, partly franked or unfranked. Fully franked dividends are ones where the whole amount of the dividend carries a franking credit, which means the company has paid 100% of the tax on the dividend and you will be able to take this as a tax offset. Partly franked dividends have only had part of the tax paid, and unfranked dividends have not had any tax paid on them, so you will need to cover this in your tax return.

.png?width=55&height=48&ext=.png)

-1.svg)